Content Specification Outlines Certified Management Accountant(CMA?)Examinations

美國(guó)注冊(cè)管理會(huì)計(jì)師(CMA?)考試內(nèi)容大綱2024年9月1日生效

The content specification outlines presented below represent the body of knowledge that will be covered on the CMA examinations.The outlines maybe changed in the future when new subject matter becomes part of the common body of knowledge.

以下內(nèi)容大綱代表了CMA考試將涵蓋的知識(shí)體系。當(dāng)新的內(nèi)容成為行業(yè)共識(shí)時(shí),大綱將會(huì)隨之更新。

Candidates for the CMA designation are required to take and pass Parts 1 and 2.

CMA認(rèn)證的考生必須參加并通過(guò)第一部分和第二部分的考試。

Candidates are responsible for being informed on the mostrecent developments in the areas covered in the outlines.This includes understanding of public pronouncements issued by accounting organizations as well as being up-to-date on recent developments reported in current accounting,financial and business periodicals.

考生有責(zé)任了解大綱所涵蓋領(lǐng)域的最新進(jìn)展。這包括理解會(huì)計(jì)組織發(fā)布的公開聲明,以及了解當(dāng)前會(huì)計(jì),財(cái)務(wù)和商業(yè)期刊中有關(guān)報(bào)告的最新進(jìn)展。

The content specification outlines serve several purposes.The outlines are intended to:

考試內(nèi)容大綱有多項(xiàng)用途。本大綱旨在:

?Establish the foundation from which each examination will be developed.

奠定考試的基礎(chǔ)。

?Provide abasis for consistent coverage on each examination.

為每次考試范圍的一致性提供基礎(chǔ)。

?Communicate to interested parties more detail as to the content of each examination part.

詳述考試各部分的內(nèi)容。

?Assist candidates in their preparation for each examination.

協(xié)助考生準(zhǔn)備各部分考試。

?Provide information to those who offer courses designed to aid candidates in

preparing for the examinations.為考試培訓(xùn)機(jī)構(gòu)提供參考信息。

Important additional information about the content specification outlines and the examinations is listed below.

下面列出了有關(guān)內(nèi)容大綱和考試的其他重要信息。

1.The coverage percentage given for each major topic within each examination part represents the relative weight given to that topic in an examination part.The number of questions presented in each major topic area approximates this percentage.

大綱中每個(gè)主題所占的百分比代表該主題在考試中的相對(duì)權(quán)重。每個(gè)主題的考題數(shù)量占總題量的比例與此權(quán)重相近。

2.Each examination will sample from the subject areas contained within each major topic area to meet the relative weight specifications.No relative weights have been assigned to the subject areas within each major topic.No inference should be made from the order in which the subject areas are listed or from the number of subject areas as to the relative weight or importance of any of the subjects.

考題的分布取決于所考察主題的相對(duì)權(quán)重。每個(gè)主題下的考點(diǎn)沒(méi)有再次分配相對(duì)權(quán)重,不應(yīng)根據(jù)考點(diǎn)的排列順序或考點(diǎn)數(shù)量來(lái)推斷其相對(duì)權(quán)重或重要

性。

3.Each major topic within each examination part has been assigned a coverage level designating the depth and breadth of topic coverage,ranging from an introductory knowledge of a subject area(Level A)to a thorough understanding of and ability to apply the essentials of a subject area(Level C).Detailed explanations of the

coverage levels and the skills expected of candidates arepresented below.

每個(gè)主題都有特定的難度水平,表示該主題所出題目的深度和廣度,可以考察從初級(jí)了解(A級(jí)難度)到透徹理解和應(yīng)用的能力(C級(jí)難度)。關(guān)于考題的難度水平和對(duì)考生能力的具體要求,之后有詳細(xì)的說(shuō)明。

4.The topics for Parts 1 and 2 have been selected to minimize the overlapping of subject areas among the examination parts.The topics within an examination part and the subject areas within topics maybe combined in individual questions.

考點(diǎn)經(jīng)過(guò)精心選擇以盡量減少第一部分考試和第二部分考試內(nèi)容的重疊??碱}可涵蓋本部分內(nèi)的主題和主題內(nèi)的相關(guān)考點(diǎn)。

5.With regard to U.S.Federal income taxation issues,candidates will be expected to understand the impact of income taxes when reporting and analyzing financial

results.In addition,the tax code provisions that impact decisions(e.g.,

depreciation,interest,etc.)will be tested.

關(guān)于美國(guó)聯(lián)邦所得稅的問(wèn)題,考生在報(bào)告和分析財(cái)務(wù)結(jié)果時(shí)應(yīng)理解所得稅的影響。此外,還將測(cè)試影響決策(例如折舊,利息等)的有關(guān)稅法規(guī)定。

6.Candidates for the CMA designation are assumed to have knowledge of the

following:preparation of financial statements,business economics,time value of money concepts,statistics,and probability.

CMA認(rèn)證的考生也應(yīng)了解財(cái)務(wù)報(bào)表編制,商業(yè)經(jīng)濟(jì)學(xué),貨幣的時(shí)間價(jià)值,統(tǒng)計(jì)和概率的有關(guān)知識(shí)。

7.Parts 1 and 2 are four-hour exams and each contains 100 multiple-choice

questions and 2 essay questions.Candidates will have three hours to complete the multiple-choice questions and one hour to complete the essay section.A small

number of the multiple-choice questions on each exam are being validated for future use and will not count in the final score.

第一和第二部分考試分別為四小時(shí),每個(gè)部分的考試包含一百個(gè)單項(xiàng)選擇題和兩個(gè)情境題。考生將有三個(gè)小時(shí)完成單項(xiàng)選擇題,一個(gè)小時(shí)完成情境題,每項(xiàng)考試中含有少數(shù)供將來(lái)使用的測(cè)試題,這些題將不會(huì)計(jì)入最終得分。

8.For the essay questions,both written and quantitative responses will be required.Candidates will be expected to present written answers that are responsive to the question asked,presented in a logical manner,and demonstrate an appropriate

understanding of the subject matter.

情境題需要語(yǔ)言論述和計(jì)算解答。要求考生以合乎邏輯的方式回答問(wèn)題,并證明對(duì)該問(wèn)題的正確理解。

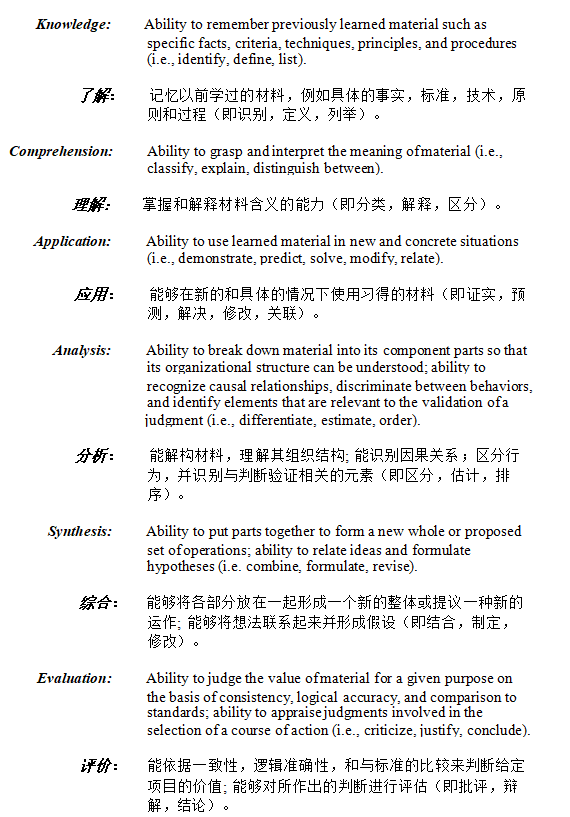

In order to more clearly define the topical knowledge required by a candidate,varying levels of coverage for the treatment of major topics of the content specification outlines have been identified and defined.The cognitive skills that a successful candidate should possess and that should be tested on the examinations can be defined as follows:

為了更清楚地定義考生所需的考點(diǎn)知識(shí),CMA考試對(duì)內(nèi)容大綱中主要考點(diǎn)確定了不同層次的能力要求。成功的考生應(yīng)具備的并將在考試中被測(cè)試的認(rèn)知能力如下所示:

The three levels of coverage can be defined as follows:

考題難度分為三個(gè)級(jí)別,分別定義如下:

Level A:Requiring the skill levels of knowledge and comprehension.

A級(jí):要求了解和理解的能力。

Level B:Requiring the skill levels of knowledge,comprehension,application,and analysis.

B級(jí):要求了解,理解,應(yīng)用和分析的能力。

Level C:Requiring all six skill levels,knowledge,comprehension,application,analysis,synthesis,and *uation.

C級(jí):要求所有六種能力,了解,理解,應(yīng)用,分析,綜合和評(píng)價(jià)的能力。

The levels of coverage as they apply to each of the major topics of the Content Specification Outlines are shown on the following pages with each topic listing.The levels represent the manner in which topic areas are to be treated and represent ceilings,i.e.,a topic area designated as Level C may contain requirements at the“A,”“B,”or“C”level,but a topic designated as Level B will not contain requirements at the“C”level.

下頁(yè)中列舉了大綱中的各主題的難度級(jí)別。所示級(jí)別為該主題考題能出現(xiàn)的最高難度,即指定為C級(jí)的主題可能出現(xiàn)“A”,“B”或“C”難度級(jí)別的題目,但指定為B級(jí)的主題不會(huì)出“C”級(jí)的題目。

Content Specification Outlines Certified Management Accountant(CMA)Examinations

注冊(cè)管理會(huì)計(jì)師(CMA)考試內(nèi)容大綱

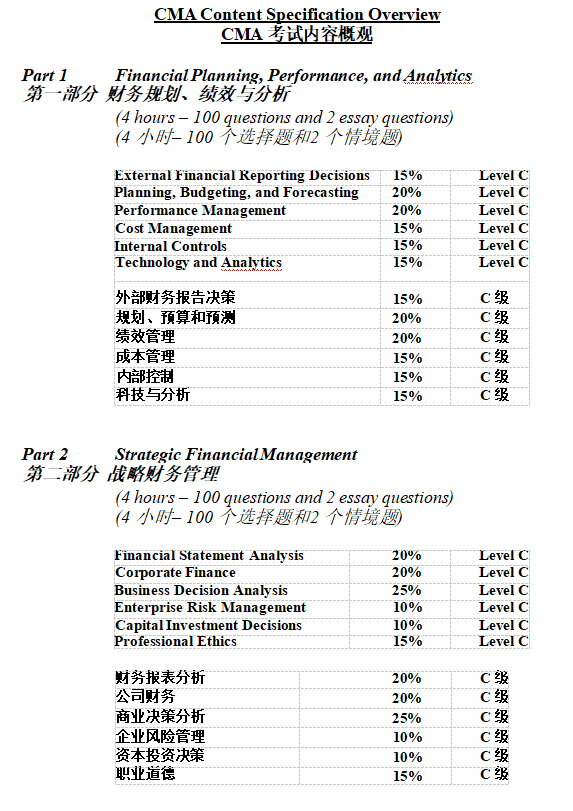

Part 1-Financial Planning,Performance,and Analytics

第一部分-財(cái)務(wù)規(guī)劃、績(jī)效與分析

A.External Financial Reporting Decisions(15%-Levels A,B,and C)

外部財(cái)務(wù)報(bào)告決策(15%-A、B和C級(jí))

1.Financial statements

財(cái)務(wù)報(bào)表

a.Balance sheet

資產(chǎn)負(fù)債表

b.Income statement

利潤(rùn)表

c.Statement of changes in equity

所有者權(quán)益變動(dòng)表

d.Statement of cash flows

現(xiàn)金流量表

e.Consolidated statements

合并報(bào)表

f.Integrated reporting

綜合報(bào)告

2.Recognition,measurement,and valuation

確認(rèn),計(jì)量,和計(jì)價(jià)

a.Asset valuation

資產(chǎn)計(jì)價(jià)

b.Valuation of liabilities

負(fù)債計(jì)價(jià)

c.Equity transactions

權(quán)益性交易

d.Revenue recognition

收入確認(rèn)

e.Income measurement

收益計(jì)量

f.Major differences between U.S.GAAP and IFRS

美國(guó)公認(rèn)會(huì)計(jì)原則與國(guó)際財(cái)務(wù)報(bào)告準(zhǔn)則的主要差異

B.Planning,Budgeting and Forecasting(20%-Levels A,B,and C)

規(guī)劃、預(yù)算和預(yù)測(cè)(20%-A、B和C級(jí))

1.Strategic Planning

戰(zhàn)略規(guī)劃

a.Analysis of external and internal factors affecting strategy

分析影響戰(zhàn)略的內(nèi)部和外部因素

b.Long-term mission and goals

長(zhǎng)期使命與目標(biāo)

c.Alignment of tactics with long-term strategic goals

根據(jù)長(zhǎng)期戰(zhàn)略目標(biāo)調(diào)整策略

d.Strategic planning models and analytical techniques

戰(zhàn)略規(guī)劃模型與分析技術(shù)

e.Characteristics of successful strategic planning process

成功的戰(zhàn)略規(guī)劃制定過(guò)程所具備的特性

2.Budgeting concepts

預(yù)算概念

a.Operations and performance goals

經(jīng)營(yíng)和業(yè)績(jī)目標(biāo)

b.Characteristics of a successful budget process

成功的預(yù)算編制流程所具備的特性

c.Resource allocation

資源分配

d.Other budgeting concepts

其他預(yù)算概念

3.Forecasting techniques

預(yù)測(cè)技術(shù)

a.Regression analysis

回歸分析

b.Learning curve analysis

學(xué)習(xí)曲線分析

c.Expected value

預(yù)期值

4.Budgeting methodologies

預(yù)算方法

a.Annual business plans(master budgets)

年度企業(yè)計(jì)劃(總預(yù)算)

b.Project budgeting

項(xiàng)目預(yù)算

c.Activity-based budgeting

作業(yè)預(yù)算編制

d.Zero-based budgeting

零基預(yù)算法

e.Continuous(rolling)budgets

連續(xù)(滾動(dòng))預(yù)算

f.Flexible budgeting

彈性預(yù)算

5.Annual profit plan and supporting schedules

年度利潤(rùn)計(jì)劃和附表

a.Operational budgets

營(yíng)業(yè)預(yù)算

b.Financial budgets

財(cái)務(wù)預(yù)算

c.Capital budgets

資本預(yù)算

6.Top-level planning and analysis

頂層規(guī)劃與分析

a.Pro forma income

預(yù)計(jì)損益表

b.Financial statement projections

預(yù)計(jì)財(cái)務(wù)報(bào)表

c.Cash flow projections

預(yù)計(jì)現(xiàn)金流量

C.Performance Management(20%-Levels A,B,and C)

績(jī)效管理(20%-A、B和C級(jí))

1.Cost and variance measures

成本與差異核算

a.Comparison of actual to planned results

實(shí)際結(jié)果與預(yù)期結(jié)果對(duì)比

b.Use of flexible budgets to analyze performance

使用彈性預(yù)算分析績(jī)效

c.Management by exception

例外管理

d.Use of standard cost systems

標(biāo)準(zhǔn)成本系統(tǒng)的使用

e.Analysis of variation from standard cost expectations

對(duì)預(yù)期的標(biāo)準(zhǔn)成本的差異分析

2.Responsibility centers and reporting segments

責(zé)任中心和報(bào)告部門

a.Types of responsibility centers

責(zé)任中心的種類

b.Transfer pricing

轉(zhuǎn)移定價(jià)

c.Contribution margin

邊際貢獻(xiàn)

d.Reporting of organizational segments

組織各部門的報(bào)告書

3.Performance measures

績(jī)效考核

a.Product profitability analysis

產(chǎn)品獲利能力分析

b.Business unit profitability analysis

經(jīng)營(yíng)單位獲利能力分析

c.Customer profitability analysis

客戶獲利能力分析

d.Return on investment(ROI)

投資回報(bào)率

e.Residual income

剩余收益

f.Investment base issues

投資基準(zhǔn)問(wèn)題

g.Key performance indicators(KPIs)

關(guān)鍵績(jī)效指標(biāo)

h.Balanced scorecard

平衡記分卡

D.Cost Management(15%-Levels A,B,and C)

成本管理(15%-A、B和C級(jí))

1.Measurement concepts

計(jì)量概念

a.Types of cost and cost behavior

成本類型和成本習(xí)性

b.Actual and normal costs

實(shí)際成本和正常成本

c.Standard costs

標(biāo)準(zhǔn)成本

d.Absorption(full)costing

吸收(全部)成本法

e.Variable(direct)costing

變動(dòng)(直接)成本法

f.Joint and by-product costing

聯(lián)產(chǎn)品和副產(chǎn)品成本法

2.Costing systems

成本計(jì)算系統(tǒng)

a.Job order costing

分批成本法

b.Activity-based costing

作業(yè)成本法

c.Life-cycle costing

生命周期成本法

d.Other costing systems

其他成本系統(tǒng)

3.Overhead costs

間接成本

a.Fixed and variable overhead expenses

固定和變動(dòng)間接費(fèi)用

b.Corporate vs.departmental overhead

公司和部門間接費(fèi)用

c.Determination of allocation base

分?jǐn)偦A(chǔ)的確定

d.Allocation of service department costs

服務(wù)部門成本的分?jǐn)?/div>

4.Supply chain management

供應(yīng)鏈管理

a.Lean resource management techniques

精益制造資源管理技術(shù)

b.Enterprise resource planning(ERP)

企業(yè)資源計(jì)劃

c.Capacity management and analysis

產(chǎn)能管理和分析

5.Business process improvement

業(yè)務(wù)流程改進(jìn)

a.Value chain analysis

價(jià)值鏈分析

b.Value-added concepts

增值概念

c.Process analysis,redesign,and standardization

流程分析,再設(shè)計(jì),和標(biāo)準(zhǔn)化

d.Continuous improvement concepts

持續(xù)改進(jìn)概念

e.Benchmarking and best practice analysis

標(biāo)桿分析和最佳實(shí)踐分析

g.Cost of quality analysis

質(zhì)量成本分析

E.Internal Controls(15%-Levels A,B,and C)

內(nèi)部控制(15%-A、B和C級(jí))

1.Governance,risk,and compliance

管理,風(fēng)險(xiǎn)與法規(guī)遵守

a.Internal control structure and management philosophy

內(nèi)部的控制結(jié)構(gòu)和管理理念

b.Internal control policies for safeguarding and assurance

保護(hù)和保證的內(nèi)部控制政策

c.Internal control risk

內(nèi)部控制風(fēng)險(xiǎn)

d.Testing methods for internal controls

內(nèi)部控制測(cè)試方法

e.Control deficiency remediation

控制缺陷補(bǔ)救

f.Corporate governance

公司治理

g.External audit requirements

外部審計(jì)規(guī)要

2.Systems controls and security measures

系統(tǒng)控制和安全措施

a.General accounting system controls

普通會(huì)計(jì)系統(tǒng)控制

b.Application and transaction controls

應(yīng)用控制和交易控制

c.Technology controls

技術(shù)控制

d.Backup controls

安全備份管控

e.Business continuity planning

業(yè)務(wù)連續(xù)性計(jì)劃

F.Technology and Analytics(15%-Levels A,B,and C)

科技與分析(15%-A、B和C級(jí))

1.Information systems

信息系統(tǒng)

a.Accounting information systems

會(huì)計(jì)信息系統(tǒng)

b.Enterprise resource planning systems

企業(yè)資源計(jì)劃系統(tǒng)

c.Enterprise performance management systems

企業(yè)績(jī)效管理系統(tǒng)

2.Data governance

數(shù)據(jù)管控

a.Data policies and procedures

數(shù)據(jù)政策和程序

b.Lifecycle of data

數(shù)據(jù)生命周期

c.Data management

數(shù)據(jù)管理

d.Controls against security breaches

控制安全漏洞

3.Technology-enabled finance transformation

技術(shù)支持的財(cái)務(wù)轉(zhuǎn)型

a.System development life cycle

系統(tǒng)開發(fā)生命周期

b.Process automation

工序自動(dòng)化

c.Innovative applications

創(chuàng)新應(yīng)用

4.Data analytics

數(shù)據(jù)分析

a.Business intelligence

商業(yè)智能

b.Data mining

數(shù)據(jù)挖掘

c.Types of data analytics

數(shù)據(jù)分析類型

d.Data visualization

數(shù)據(jù)可視化

點(diǎn)擊直接下載pdf版本:注冊(cè)管理會(huì)計(jì)師(CMA)考試內(nèi)容大綱

-

關(guān)注公眾號(hào)

報(bào)考咨詢 專業(yè)師資

考前資料下載

- 贊1265